List of Video Courses

Asset Liability Management

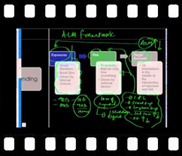

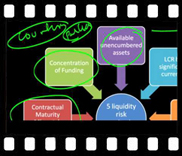

The Asset Liability Management (ALM) & Capital Adequacy course looks at the overall ALM framework and various tools and reports that address the impact of interest rate changes to shareholder value and interest income sensitivity. A historical review of capital adequacy regulation is also presented from Regulation Q to Basel II to the liquidity risk extensions of Basel III.

|

|

|

||

|

|

|

||

| Back to top | ||||

Calculating VaR (Value at Risk)

The “Calculating VaR” course walks through the various VaR methodologies; specific calculations for a multiple currency and commodity portfolio using an excel worksheet; questions that the measure can provide an answer to; a real-world case study; and the qualifications and limitations of using the VaR measure.

|

|

|

||

|

|

|||

| Back to top | ||||

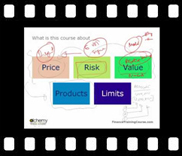

Cross Selling Treasury Products

The “Cross Selling Treasury Products” course presents a framework for empowering client facing treasury teams to go out and cross sell high value, high margin trading concepts to clients by educating customers about their exposures and presenting some of the solutions available to reduce the risk associated with those exposures.

Our discussion revolves around 5 core themes: Price, Risk, Value, Products and Limits. We also present a case-study, relating to the Petrochemical industry, to illustrate the framework. We wrap up the course first with an overview of the core products typically used in a Treasury along with customer reactions to those solutions, and then with a review of vanilla and exotic derivative products.

|

|

|

||

|

|

|||

| Back to top | ||||

Option Pricing using Binomial Trees

The “Option Pricing using Binomial Trees” course first walks through the conventional binomial tree approach for pricing options and then through an alternative method. The latter is based on the techniques documented by Professor Mark Broadie of Columbia Business School as part of his coursework in Security Pricing and Computational Finance courses at Columbia University. Examples of its application to pricing vanilla and exotic options are provided. The methodology allows for extending a simple 3-step tree to a 50 – 100 step option pricing tree in a few minutes to improve result accuracy.

|

|

|

||

|

|

|||

| Back to top | ||||

Option Pricing using Monte Carlo Simulation

The “Option Pricing using Monte Carlo Simulation” course helps to build a better understanding of N(d1) and N(d2), the risk-adjusted probability functions in the Black-Scholes option pricing formula, with the aid of a simulator. The course then focuses on demonstrating the steps for building a Monte Carlo simulator in Excel that can be used to price some exotic option contracts.

|

|

|

||

|

|

|

||

|

||||

| Back to top | ||||

Quant Crash Course

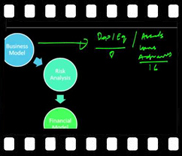

The “Quant Crash Course” covers volatility, value at risk, capital and limit management frameworks for a treasury function. It explains the essential elements of a given distribution; considers volatility and correlation in relation to a valuation and risk management or control system; discusses the importance of duration and convexity to the risk management process; reviews Value at Risk (VaR) including its various applications and limitations; demonstrates how a risk framework may be built around capital and reviews an ICAAP model framework and a limits management process; and discusses various limits such as counterparty (including Pre-settlement risk), transaction, exposure and sensitivity limits.

|

|

|

||

|

|

|

||

|

||||

| Back to top | ||||

Selling Derivatives Products

The “Selling Derivatives Products” course is an introductory course for beginners with simple examples explaining vanilla derivative products as well as the differences between forwards, futures and options. The course also provides an overview of the core products typically used in a Treasury function along with TMU customer reactions to those solutions.

|

|

|||

| Back to top | ||||

Setting Value at Risk (VaR), Stop Loss, Pre Settlement (PSR) and Counterparty Limits

The “Setting Value at Risk (VaR), Stop Loss, Pre Settlement Risk (PSR) and Counterparty Limits” course first provides a theoretical overview of Value at Risk as well as the limitations of this measure. Various VaR calculation methodologies are discussed and the procedure for determining portfolio VaR is reviewed. This is followed by a discussion on how VAR is used in allocating, calculating and defining optimal levels for limits: Stop Loss Limits, Pre-Settlement Risk (PSR) Limits and Margin haircuts for bonds; how to set up stop loss thresholds; how a financial institution’s board of directors interprets and assesses the credibility of VAR results; and how Stop Loss may be calibrated to the VaR threshold.

|

||||

| Back to top | ||||

Stress Testing

The “Stress Testing” course review the concepts of stress testing, risk capital, value at risk, asset liability management and capital adequacy applications for stress testing. The course covers the he need for stress testing, stress testing capital and stress testing methodology / framework for price risk, credit risk, interest rate mismatch & ALM as well looks at various ALM reports. Related topics, included as part of this course, are the Calculating Value at Risk Course, Understanding Capital, a review of the evolution of Capital Adequacy requirements and ICAAP, Basel II and Basel III’s liquidity extensions, and the linkage between optionality, volatility, duration and convexity.

|

|

|

||

|

|

|

||

|

|

|

||

| Back to top | ||||

Understanding N(d1) and N(d2)

The “Understanding N(d1) and N(d2)” course provides a theoretical overview of the interpretation of and an explanation for the difference between the risk-adjusted probabilities of the Black-Scholes option pricing formula as well as demonstrates the same practically with the aid of a Monte Carlo simulation model.

|

|

|

||

| Back to top | ||||