| The “ALM and Capital Adequacy Course” serves as an introduction as well as a refresher course to Asset Liability Management. The course is divided across a number of core topics from basic concepts such as duration and convexity to more advanced topics such as ALM measurement tools. The following topics are covered in the course: |  |

- Introduction to ALM

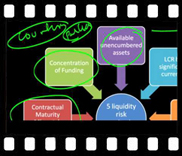

- Interest Rate/ Maturity Mismatch Risk and Liquidity Risk

- Duration and Convexity, including the relationship with options and volatility

- Asset and Liability Sensitivity

- ALM framework

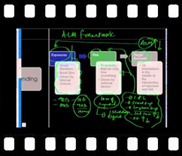

- Building blocks for an ALM model

- ALM measurement tools

- ALM reporting

- ALM Stress Testing

- Introduction to Capital Adequacy (including a background of capital adequacy regulation)

- Internal Capital Adequacy Assessment Process (ICAAP) & Liquidity Risk Capital Extensions

Course Prerequisites

Familiarity with basic asset liability management concepts, value-at-risk (VaR), local markets, portfolio management and the Basel II framework.

Course Audience

The course is targeted to intermediate and advanced users and is aimed primarily at banking professionals and individuals responsible for asset liability management and risk management within banks, insurance companies and mutual funds who need to quickly review or refresh their understanding of ALM and Capital Adequacy regulations for work, professional review, audit or personal development.

Course Guide

Here is the structure of the course.

|

Title

|

Duration

|

||

| Session 1 – Introduction to Asset Liability Management (ALM) | 33:15 mins | ||

| Session 2 – Interest Rate mismatch & ALM | 21:51 mins | ||

| Session 3 – ALM reports and extensions | 26:59 mins | ||

| Session 4 – Evolution of Capital Adequacy requirements | 16:32 mins | ||

| Session 5 – Review of ICAAP (Internal Capital Adequacy Assessment Process) & Basel II (III) – Liquidity risk adjustments | 34:06 mins | ||

| Session 6 – Understanding Duration & Convexity | 22:58 mins | ||

Session One – Introduction to Asset Liability Management (ALM) | ||

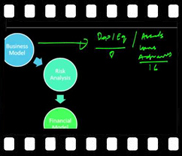

| After covering market (price) risk and credit risk, it is now time to take a look at Interest Rate Risk or Maturity Mismatch risk. Before we move on to the topic of bank capital adequacy it is important that we have a good grip on what drives Interest Rate Mismatch and Liquidity risk at a bank.We use Asset Liability Management as a tool to measure interest rate exposure and introduce the concept of maturity mismatch at a high level. This is quickly followed by an introduction to a simplified ALM framework that we will use as a foundation for the ALM stress testing report we will use in later sessions. |  | |

Session Two: Asset Liability Management (ALM) | ||

| We continue with more core definitions and introduce the primary questions an ALM framework is expected to answer covering both shareholder value and interest income sensitivity. Starting with duration and convexity we introduce the concept of Asset Sensitivity and Liability Sensitivity before walking through the core steps required for building an ALM model. |  | |

Session Three: Asset Liability Management (ALM) Reports | ||

| In our last and final session on ALM, we introduce and walk through the Maturity and Rate GAP reports and use them to build and introduce the Earnings at Risk and Market Value of Equity at Risk reports. The session uses an Excel based template to walk participants through the 4 report format, their usage and applications. |  | |

Session Four: Introduction to Capital Adequacy | ||

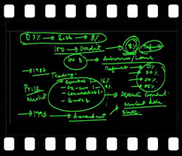

| In our refresher on capital adequacy, we review the origins of capital adequacy regulation and margin of safety in banks starting with Regulation Q and the evolution of the Basel I and Basel II standards over the last 30 years. |  | |

Session Five: ICAAP (Internal Capital Adequacy Assessment Process) and Liquidity Risk Capital extensions | ||

| We review Pillar I, Pillar II requirements as well as a quick walk through the ICAAP (Internal Capital Adequacy Process) and the Basel II liquidity risk extensions. Briefly touch liquidity coverage ratio, net stable funding ratio and integrating correlations within stress testing. |  | |

Session Six: Understanding Duration & Convexity | ||

| We review duration and convexity; the alternative definition of convexity and its importance to the risk management process, the relationship between options, convexity and volatility. |  | |

| Back to top |